2024 Reverse Mortgage Purchase Guide: Rates, Limits & Down Payment

|

Michael G. Branson, CEO of All Reverse Mortgage, Inc., and moderator of ARLO™, has 45 years of experience in the mortgage banking industry. He has devoted the past 19 years to reverse mortgages exclusively. (License: NMLS# 14040) |

|

All Reverse Mortgage's editing process includes rigorous fact-checking led by industry experts to ensure all content is accurate and current. This article has been reviewed, edited, and fact-checked by Cliff Auerswald, President and co-creator of ARLO™. (License: NMLS# 14041) |

Michael G. Branson

Michael G. Branson Cliff Auerswald

Cliff AuerswaldReverse mortgages are a popular choice for individuals looking to remain in their homes as they age. However, a unique variant—the Reverse Mortgage Purchase—enables borrowers to buy a new home without paying all cash or taking a traditional mortgage.

Opting for a Reverse Mortgage Purchase can be particularly beneficial for various life situations.

Many find it an appealing option when considering the following:

- The desire to downsize to a more manageable home, reducing the burden of upkeep.

- The preference for a single-level dwelling that can better accommodate the needs of aging in place.

- The need to move closer to family, ensuring support is within reach.

With a Reverse Mortgage for Purchase, often facilitated by the Home Equity Conversion Mortgage (HECM) for Purchase program, you can streamline the process, allowing you to secure a reverse mortgage and acquire a new residence seamlessly.

Reverse Mortgage Purchases Basics

The HECM for Purchase is the most common reverse mortgage borrowers use to purchase new homes. Applying for and qualifying for a HECM for Purchase follows the same process as applying for any HECM loan.

Most requirements are the same:

Borrowers must be 62 or older and qualify under the HUD financial assessment guidelines. Instead of having equity in a home, borrowers must be able to put down a sizeable down payment, with the reverse mortgage covering the rest (with no monthly mortgage payments).

After completing a HECM for Purchase, borrowers must maintain the home to FHA standards and pay property taxes and homeowners’ insurance in a timely manner as well as any other property charges (i.e., HOA dues, etc.). The main difference between using a reverse mortgage for purchase and getting a reverse mortgage later is that with the purchase, it is all one transaction, and therefore, there are no duplicate fees.

The reverse mortgage for purchase product requires the borrower to cover the down payment on the new home purchase, which includes the required mortgage insurance that may be more a typical conventional home mortgage purchase but is still less than a purchase of any type and a reverse mortgage refinance later.

So, if your plans call for a reverse mortgage, a single reverse mortgage purchase is much better than a purchase and a subsequent refinance.

Eligible Properties

- Single-family homes

- PUD – planned unit development

- 2–4-unit dwelling

- HUD-approved condominiums

In all cases of new construction, a certificate of occupancy must be in place before the HECM for a purchase transaction. Most property types can be purchased in a reverse mortgage, with several exceptions.

Ineligible Properties

The home must not be under construction and must be habitable. Co-ops, boarding houses, B&Bs, and newly constructed homes where a Certificate of Occupancy has yet to be issued are ineligible.

Certain types of manufactured homes may not qualify for reverse mortgage financing. Those built before 1976 will not.

HUD publishes its minimum standards for manufactured homes, and any properties that do not meet those standards are ineligible for a reverse purchase mortgage.

Estimating Your Down Payment

The reverse mortgage for purchase program requires the borrower to cover the down payment on the new home purchase. The down payment requirement for a purchase with a reverse mortgage is higher than most other types of financing, but then borrowers have no required monthly payments.

In many cases, borrowers use the equity from the sale of their existing house for the down payment on the new home. In other cases, the borrower may need to cover the down payment through savings or other means.

If the value of the old home is less than the down payment required for the new home, the borrower will need to provide the difference in cash. Some gifts and other sources may also be allowed under FHA requirements, such as family gifts from those who do not have a stake in the transaction.

If you need to use gift funds, you should always discuss with your lender so that you can verify the requirements for gift fund verification and eligibility in advance.

The down payment requirement is based on the following:

- The age of the youngest borrower

- Current interest rates

- The price of the new home, or the HECM lending limit of $1,149,825

Typically, the down payment for a HECM for Purchase is 45-70% of the purchase price. The following table provides examples of down payment requirements for various home prices and borrower ages.

HECM Purchase Down Payment Estimates by Age and Home Value

Please note that this is not a lending offer. The down payment figures provided are estimates, inclusive of the majority of essential closing costs, such as a 2% upfront mortgage insurance fee and third-party closing costs. These estimates are based on an interest rate of 6.93%, which includes an expected rate of 6.10% and an adjustable CMT margin of 1.625%, accurate as of December 4, 2023.

Age % Down $200,000 $400,000 $600,000 $800,000 $1,00,0000

62 67.2% $134,400 $268,800 $403,200 $537,600 $672,000

65 65.1% $130,200 $260,400 $390,600 $520,800 $651,000

70 61.4% $122,800 $245,600 $368,400 $491,200 $614,000

75 58.5% $117,000 $234,000 $351,000 $468,000 $585,000

80 54.1% $108,200 $216,400 $324,600 $432,800 $541,000

85 47.9% $95,800 $163,600 $287,400 $383,200 $479,900

90 40.9% $81,800 $163,600 $245,400 $327,200 $400,900

Today's Reverse Mortgage Purchase Rates

Example calculation using fixed rate:

2024 Lending Limit Fixed Rate Adjustable Rate

$1,149,825 7.180% (8.700% APR) 6.885% (2.125 Margin)

$4,000,000 10.125% (10.612% APR) 11.385% (6.625 Margin)

7.18% + .50% Monthly MIP = 7.68% in total interest charges. Fixed Rate APR calculated assumes a $250,000 loan amount and includes .50% Mortgage Insurance and standard 3rd party closing costs.

Sourcing Your Down Payment

- Cash on hand (Savings, 401k, etc.)

- Proceeds from the sale of the home

- Gift from family

Proceeds from the sale of the previous home and savings are the most common ways for borrowers to meet the down payment requirement. There are other acceptable funding sources under the Federal Housing Administration, which is the insurer for the loan.

For sources that will work to finance the equity portion of the loan, borrowers can use an earnest money deposit or a withdrawal from a savings account, checking account, or retirement fund.

Some forms of gift money are also OK, including gifts from family members, employers, a charity, a government organization interested in home ownership initiatives, or a close friend with a documented interest in the borrower. All funds need to be verified.

Gifts from someone involved in the transaction, in any way, are not acceptable. Other less common funding sources, such as collateralized loans, savings bonds, employer assistance programs, and other means, can also be used.

Down Payment Sources You Can’t Use

Sweat equity, trade equity, rent credit, and cash from someone benefiting from the reverse mortgage transaction are unacceptable. Cash advances from credit cards are also not accepted.

Example of Reverse Mortgage Purchase

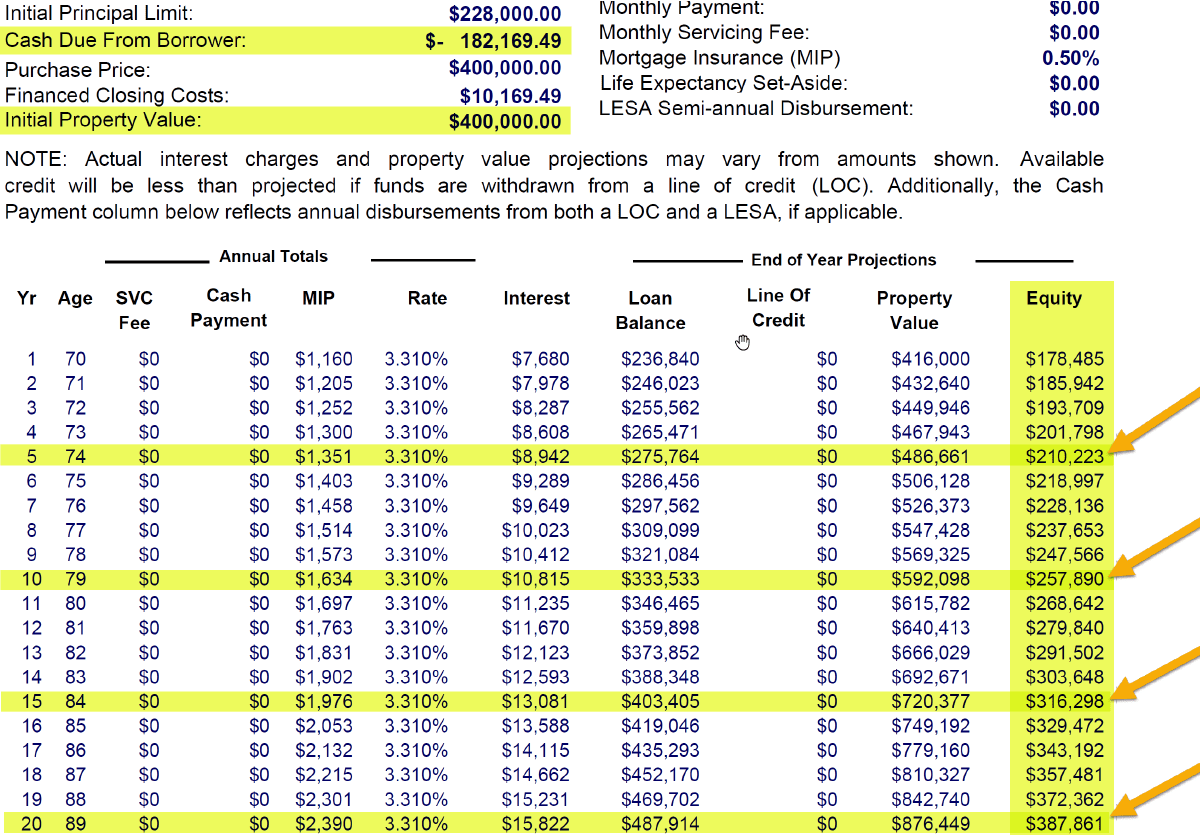

In this example, we will use a 70-year-old borrower with a reverse mortgage to purchase a home with a sales price of $400,000. The required down payment is $182,000, or approximately 45% of the purchase price.

No one can foretell interest rates or how much your home will appreciate over the years, so estimates are prepared using a 4% annual appreciation of the home, and the interest is calculated using an “expected rate” based on a 10-year index and not the lower index from which you begin to accrue interest.

Many properties appreciate more than 4% annually, but 4% is a solid, relatively conservative number. If you feel your home will appreciate more or less, you may want to keep that in mind while considering the numbers.

The down payment includes all upfront mortgage insurance premiums and third-party closing costs. After five years of making no mortgage payments, there would be $210,000 in home equity; after 10 years, there is still $257,000 based on the abovementioned assumptions.

Should the borrower decide to move into an assisted care facility later, the loan would become due and payable, but the borrower or their family can sell the home. The home and any equity in the home over the outstanding loan balance always belongs to the borrower and their heirs.

They can pay the loan off and keep the house, sell the home and keep the proceeds, or, in some cases, walk away and owe nothing.

The remaining equity largely depends on the home’s future appreciation, interest rates, the amount and timeliness of reverse mortgage funds drawn (which are 100% at inception on a purchase), and whether or not the borrower makes any early voluntary repayments.

Also See: Here’s an Ideal Reverse Mortgage Purchase Example

Advantages and Disadvantages of Reverse Mortgage Purchases

The HECM purchase program can be an excellent option for those who want to move during retirement, as it allows them to do so without making monthly mortgage payments. However, like all loans, there are some pros and cons.

Additional Considerations

Another factor that borrowers may want to consider in purchasing with a reverse mortgage is the real estate agent’s experience with reverse mortgages. While the mortgage originator can help answer questions along the way, borrowers may want to work with a real estate agent familiar with reverse mortgage transactions.

Purchase FAQs

Can you get a reverse mortgage on a purchase?

How does a reverse mortgage purchase work?

How much is the down payment required on a reverse mortgage purchase?

The amount of down payment required will depend on the borrower’s loan eligibility as determined by the HUD calculator. This determination is based on a calculation of factors such as the age of the youngest borrower/spouse, the interest rate, and the HUD lending limit to determine the HUD Principal Limit. The Principal Limit is the amount that the reverse mortgage will advance toward the transaction, and the borrower(s) would need to bring in the rest to complete the transaction. For example, a 62-year-old borrower may be eligible for a loan-to-value percentage of ~36%. A 92+-year-old borrower may be eligible for a ratio of ~65%, to which the borrower would also need to add any fees. Curious about your down payment? Try our reverse mortgage for purchase calculator.

How is a reverse mortgage purchase different from a traditional mortgage?

Can you use a reverse mortgage purchase loan and then move to a nursing home?

Can I purchase a multifamily with a reverse mortgage and live in one of the units?

How can I find realtors who understand HECM for purchase?

Does the reverse mortgage purchase appraisal need to be near the asking price or just over the loan amount?

Can I use funds from a cash-out refinance for the down payment on a HECM purchase?

Are condos eligible for the purchase reverse mortgage?

Can I purchase with a reverse mortgage if I had a bankruptcy 3 years ago?

Can my spouse use a reverse mortgage to purchase the home as the sole owner?

Can you sell the house, and if so, are there time constraints or limitations?

Is it possible to sell a home with an existing reverse mortgage and use the proceeds to buy a new one with a new reverse mortgage, allowing both transactions to close simultaneously?

How can I use a life insurance policy to get the cash necessary for the down payment on HECM for purchase?

2024 Purchase Changes & Improvements

- Assistance with Borrower’s Fees: Now, parties involved in the home buying process (like sellers, agents, and builders) can contribute up to 6% of the home’s cost to help with various fees.

- Uses of the 6% Contribution: This amount can cover expenses such as origination fees, closing costs (including credit reports and appraisals), prepaid items, discount points, interest rate reductions, and the initial mortgage insurance premium. However, it cannot be used for counseling fees.

- Additional Funding Options: In addition to the HECM loan, you can use other sources, such as premium pricing, gifts, disaster relief grants, and employer assistance, to fund your share of the purchase.

- Premium Pricing Credits: Deals from mortgage companies or third-party originators are exempt from the 6% limit, provided they are not the seller, agent, builder, or developer.

- Seller-Related Fees: Usual seller fees, such as real estate commissions and home warranty costs, are permitted and do not count towards the 6% limit.

- PACE Liens: Clearing a Property Assessed Clean Energy (PACE) lien by the seller is not considered an interested party contribution under this program.

These updates make buying a home easier under the HECM for Purchase program by allowing more financial support from various sources.

For More Information:

- Check the FHA Single Family Housing Policy Handbook at Hud.gov.

- Refer to the Federal Register for detailed updates.

ARLO recommends these helpful resources:

- Read about our own HECM Purchase client success story in Kiplinger’s Retirement Report

HECM Purchase YouTube Series

Have a Question About Reverse Mortgages?

March 17th, 2024

March 19th, 2024

August 10th, 2021

August 10th, 2021

November 24th, 2020

November 24th, 2020

May 26th, 2020

May 26th, 2020

January 14th, 2013

January 15th, 2013

November 26th, 2012

December 4th, 2012